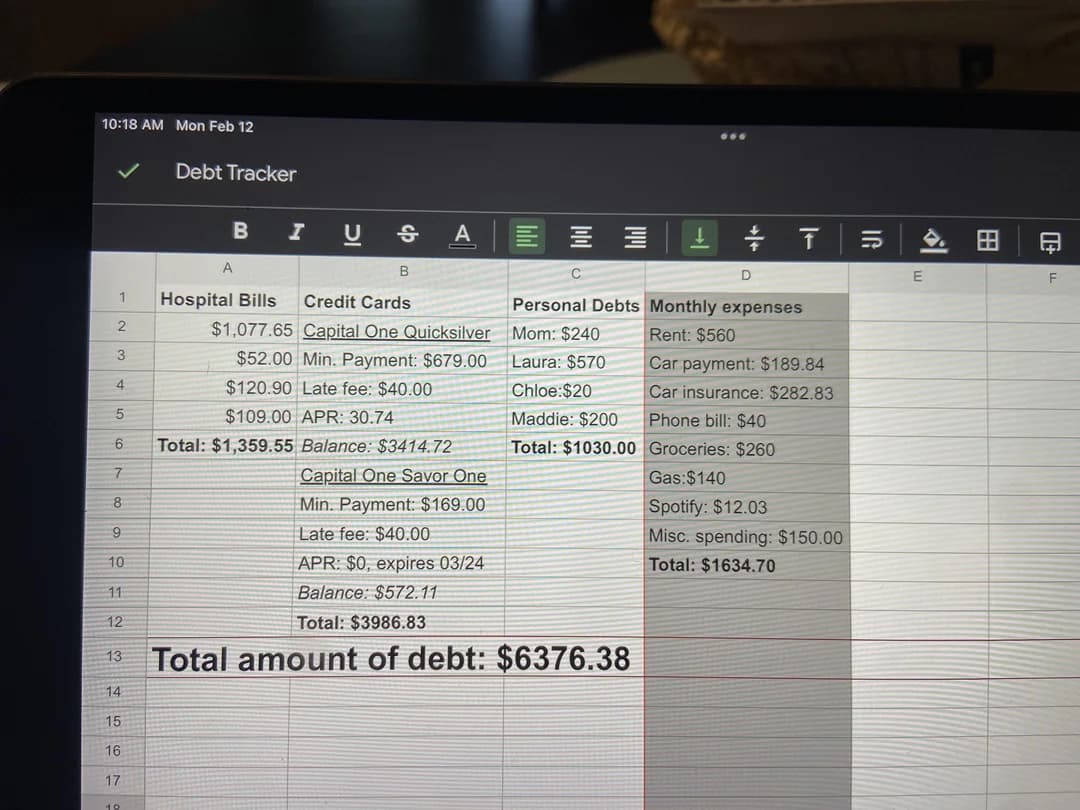

I’m 21 and have racked up $6,376.38 in debt. This includes credit cards, personal loans from friends and family, and medical bills. I was in and out of jobs for a while, which made things really tough, but now I have a new job making $28.20 an hour and a part-time job that brings my monthly income to about $3,000. My expenses are listed in a spreadsheet, and I’ve started setting aside $50 per paycheck into savings, so I’ll save at least $100 a month. What’s the best way to tackle this? Should I start with credit cards or personal loans? Any tips would be amazing.

That car insurance seems really high. Did you shop around, or did you just go with the first quote? Also, you should focus on paying off your credit cards based on their APR. Start with the 30% APR one, then move to the 0% one before its promo ends. The interest on these can pile up fast.

@Lex

Why is car insurance so expensive for OP?

Sullivan said:

@Lex

Why is car insurance so expensive for OP?

I’m a young driver, plus I have a car accident on my record, so yeah, it’s expensive. I’ve tried looking for cheaper rates, but it’s tough.

Pay off the 0% credit card before the promo ends. After that, tackle the card with the highest interest rate. Leave the hospital bills and personal loans for last—they’re not charging interest, so there’s less urgency.

@Ainsley

I get the math, but honestly, I’d start with paying back friends and family first. It feels better to clear those personal debts quickly.

@Ainsley

Why focus on the 0% card first? Isn’t it smarter to pay off the one with the highest APR?

Mai said:

@Ainsley

Why focus on the 0% card first? Isn’t it smarter to pay off the one with the highest APR?

If you don’t pay off the 0% card before the promo ends, you could get hit with deferred interest. That’s why it’s good to clear it first.

@Luca

Actually, most regular credit cards don’t charge deferred interest. You just start accruing interest from the expiration date forward. Deferred interest is more common with store cards.

@Luca

That makes sense! Thanks for explaining.

You could probably put around $1,300 per month towards your debt based on your budget. Start with paying off friends and family, then build a $1,000 emergency fund. Once that’s done, hit the credit cards, starting with the one with the highest APR.

@Dru

I really like this plan. I want to pay off personal debts quickly since I hate owing people close to me. I also want to build up my savings.

Kit said:

@Dru

I really like this plan. I want to pay off personal debts quickly since I hate owing people close to me. I also want to build up my savings.

You could even offer to pay back personal loans with a little extra—like $10 or $20 as a gesture of goodwill. It might help if you ever need to borrow again.

@Dru

Does this plan include making minimum payments on your credit cards while paying off friends and family?

Meade said:

@Dru

Does this plan include making minimum payments on your credit cards while paying off friends and family?

Good catch—yes, always make the minimum payments to avoid fees or penalties. After that, focus on personal debts and savings.

Clear the 0% card before the promo ends. After that, tackle the personal loans—it’s only fair to pay back the people who helped you.

Here’s what I’d do: 1) Pay off the 0% card before the promo ends. 2) Decide between the high-interest card and personal debts based on what feels more urgent to you—financially, the credit card makes more sense, but relationships matter too. 3) Leave medical bills for last; you can usually negotiate them down.

Cut back wherever you can. Cancel non-essentials like Spotify for a few months and put that money toward personal debts. For medical bills, call the provider and ask for a payment plan or financial assistance.

@Vega

I’ve already cut back a lot. Spotify helps me stay sane, so I think I’ll keep it. But I’ll look into negotiating the medical bills—thanks for the advice!

Shop around for cheaper car insurance every year. You might save a ton, especially if you bundle with other policies.