Hi everyone, I’m a 34-year-old with a wife and young daughter. I’ve ended up in a lot of debt after losing control of my spending. I make about $1,650 a month, and after covering rent, bills, and food, I barely have anything left. Right now, I’m only paying the MBA card, which will be paid off by May, leaving me $420 to start tackling other debts. My wife stays home to care for our daughter, but we’re considering how she might bring in extra income. I plan to contact the banks to discuss refinancing or reorganizing my debt, and I’m looking for a second job to boost my income. What else can I do? This situation feels overwhelming, but I’m determined to work through it. Thanks for reading.

Your plan makes sense.

-

Contact the banks and ask if they can offer you a hardship program.

-

Focus on boosting your income with a second job.

Also, look into free resources online that offer tips for paying off debt. They could help with more strategies.

You’ll need another job or a better-paying one. $1,650 a month is tough to live on, let alone pay off debt.

I’ve seen some people mention making extra money by donating plasma. You and your wife could take turns doing that. Also, talk to the banks about hardship options or consider debt consolidation. But honestly, the main thing is figuring out how to increase your income.

Get a second or even third job. Both you and your wife might need to pitch in to make this work.

Is $1,650 your monthly income after taxes? If so, that’s very low, and you should focus on increasing it as soon as possible.

A 41% interest rate on a card? That’s crazy. Focus on paying that off first. Can you look for a higher-paying job? This will take forever on your current income unless you make some big changes. Bankruptcy might also be worth considering if it’s too overwhelming, but make sure to research it thoroughly and stick to a strict budget afterward. Best of luck—you can get through this!

You need to work on doubling up payments on the debt with the highest interest rate. Any extra income you get should go toward that too.

I’m confused—are you making $1,650 a month and have an MBA? If so, you need to find a way to earn more money. The hole is too deep otherwise.

Kiran said:

I’m confused—are you making $1,650 a month and have an MBA? If so, you need to find a way to earn more money. The hole is too deep otherwise.

I think MBA is referring to a loan or card, not an actual degree.

@Kai

Oh, that makes more sense. For a second, I thought they were saying they owed $840 on an MBA program and were only making $1,650 monthly. That would be super rough.

Kiran said:

@Kai

Oh, that makes more sense. For a second, I thought they were saying they owed $840 on an MBA program and were only making $1,650 monthly. That would be super rough.

Yeah, you got it right. It’s a loan.

- What are your minimum payments?

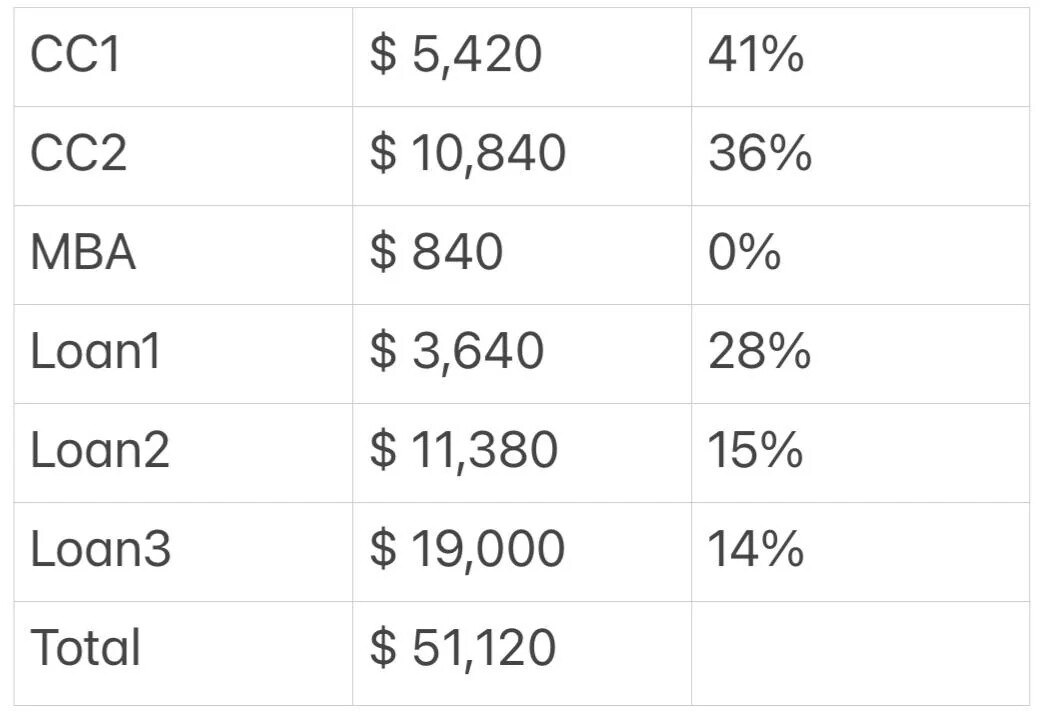

- Are the percentages listed APR or utilization rates? Because 41% APR is insane.

- Is your income monthly? If so, it sounds like minimum wage. Is that right?

Just trying to understand better so we can give good advice.

@Kai

Hi! 1. I can’t afford to pay any minimums until June, and even then, I can’t cover all of them. 2. Yes, it’s the APR. 3. My income is monthly, and it’s a bit above minimum wage.

The most efficient way to pay down debt is using either the snowball or avalanche method. Snowball focuses on paying off smaller balances first, while avalanche targets the highest interest rates. Both can work, so pick the one that feels right for you. There are tools online that can help you figure out the best approach for your situation. Hope this helps!

@Kieran

Thanks a lot for the advice!

You should focus all your extra money on the CC1 debt after making minimum payments on everything else.

Penn said:

You should focus all your extra money on the CC1 debt after making minimum payments on everything else.

It sounds like the minimum payment on the MBA card is $420, so clearing that first might make sense since it’s a big chunk of their expenses.

Those interest rates are really high.